No Early Withdrawal Tax Penalties!

Use your IRA or 401k to fund or use as a downpayment to purchase your own Business. Leverage Your Retirement to Fund Your Future: An Overview of ROBS

Click Here to Pre-qualify for business financing today!

Your results will include your maximum funding amount and a list of your pre-approved funding options.

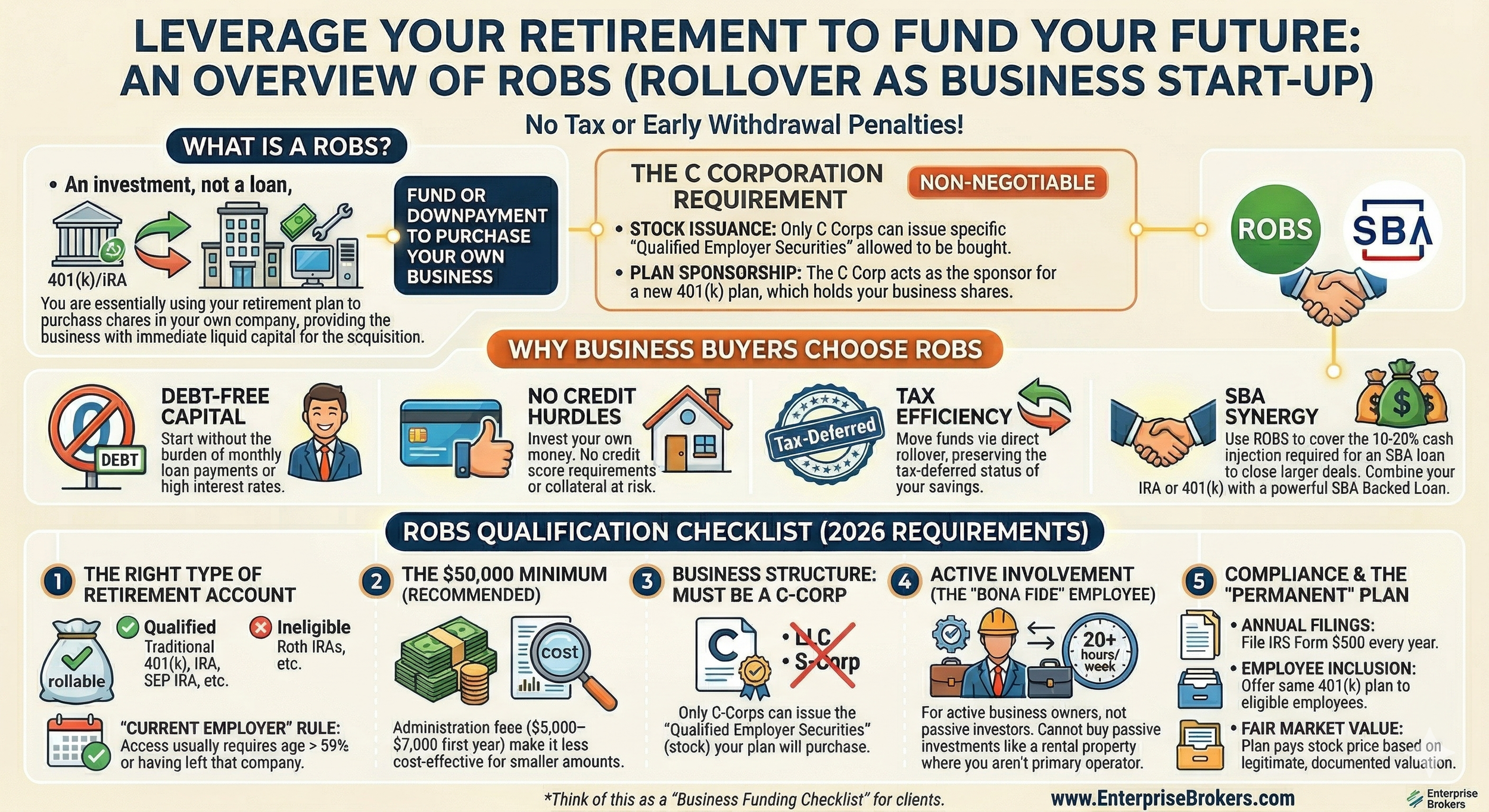

A Rollover as Business Start-up (ROBS) is a specialized financial structure that allows you to use your 401(k), IRA, or other qualified retirement funds to buy a business—without paying early withdrawal penalties or income taxes.

Unlike a traditional loan, ROBS is an investment. You are essentially using your retirement plan to purchase shares in your own company, providing the business with immediate liquid capital for the acquisition.

The C Corporation Requirement

To utilize a ROBS structure, the business must be established as a C Corporation. This is a non-negotiable legal requirement because:

Stock Issuance: Only C Corps can issue the specific type of "Qualified Employer Securities" that your retirement plan is permitted to buy.

Plan Sponsorship: The C Corp acts as the sponsor for a new 401(k) plan, which then holds the shares of your business.

Why Business Buyers Choose ROBS

Debt-Free Capital: Start your journey without the burden of monthly loan payments or high interest rates.

No Credit Hurdles: Since you are investing your own money, there are no credit score requirements or collateral (like your home) at risk.

Tax Efficiency: You move your funds via a direct rollover, preserving the tax-deferred status of your hard-earned savings.

SBA Synergy: ROBS can be used to cover the 10-20% "cash injection" required for an SBA loan, making it easier to close larger deals.

Combine your IRA or 401k with a SBA Backed Loan and you have a powerful to purchase the business of your dreams.

To qualify for a Rollover as Business Start-up (ROBS) in 2026, there are several hard requirements set by the IRS and Department of Labor.

Think of this as a "Business Funding Checklist" you can use for your clients at Enterprise Brokers.

1. The Right Type of Retirement Account

You must have a "rollable" retirement account. Most pre-tax (tax-deferred) accounts qualify, but there are exceptions:

Qualified Accounts: Traditional 401(k), 403(b), Traditional IRA, SEP IRA, SIMPLE IRA, Keogh, and TSP (Thrift Savings Plan).

The "Not" List:Roth IRAs are strictly ineligible. Inherited IRAs and 457(b) plans from non-governmental (tax-exempt) organizations also typically do not qualify.

The "Current Employer" Rule: If your funds are in a 401(k) with your current employer, you usually cannot access them unless you are over age 59½ or have left that company.

2. The $50,000 Minimum (Recommended)

While there is no legal "minimum" dollar amount, most experts recommend having at least $50,000 available to roll over.

Why? The setup and annual administration fees (typically $5,000–$7,000 for the first year) make it less cost-effective for smaller amounts.

3. The Business Structure: Must be a C-Corp

You cannot use ROBS for an LLC, S-Corp, or Sole Proprietorship. The business must be a C Corporation because: Only C-Corps can issue the "Qualified Employer Securities" (stock) that your 401(k) plan will purchase to fund the business.

4. Active Involvement (The "Bona Fide" Employee)

ROBS is for active business owners, not passive investors.

You must be a "bona fide" employee of the company (typically working 20+ hours per week or 1,000 hours per year).

You cannot use ROBS to buy a passive investment like a rental property where you aren't the primary operator.

5. Compliance & The "Permanent" Plan

Once the business is funded, you have ongoing responsibilities:

Annual Filings: You must file IRS Form 5500 every year.

Employee Inclusion: If you have eligible employees (usually those working 1,000+ hours a year), you must offer them the same 401(k) plan you used to fund the business.

Fair Market Value: The price your 401(k) plan pays for the business stock must be based on a legitimate, documented valuation.

Fill out the form below and we will put you in touch with Qualified ROBS Plan Manager.