SBA 7a and 504 Information for Florida Business Buyers and Sellers

SBA guidelines impose stricter lending and contracting rules to mitigate financial risk and ensure program integrity. These guidelines feature stringent credit score and collateral requirements, 100% U.S. ownership rules, and size/affiliation standards.

Key Guidelines and Stricter Standards

Citizenship and Ownership: Businesses must be 100% U.S. owned or owned by Legal Permanent Residents (LPRs). All new owners must co-borrow, and no undocumented immigrants may be employed by an applicant business.

Credit and Collateral: The minimum Small Business Scoring Service (SBSS) credit score is strictly enforced, and asset pledges are required for smaller loans with collateral thresholds set to $50,000.

Equity Requirements: Equity injections for business startups and change of ownership deals must be a minimum of 10%. Seller financing is capped at 50% of the deal with full standby terms.

Affiliation and Size Standards: The SBA evaluates business size based on the aggregate of the concern and its affiliates. Affiliation is determined by control, whether through majority ownership, stock options, or "negative controls" (veto power held by minority shareholders)

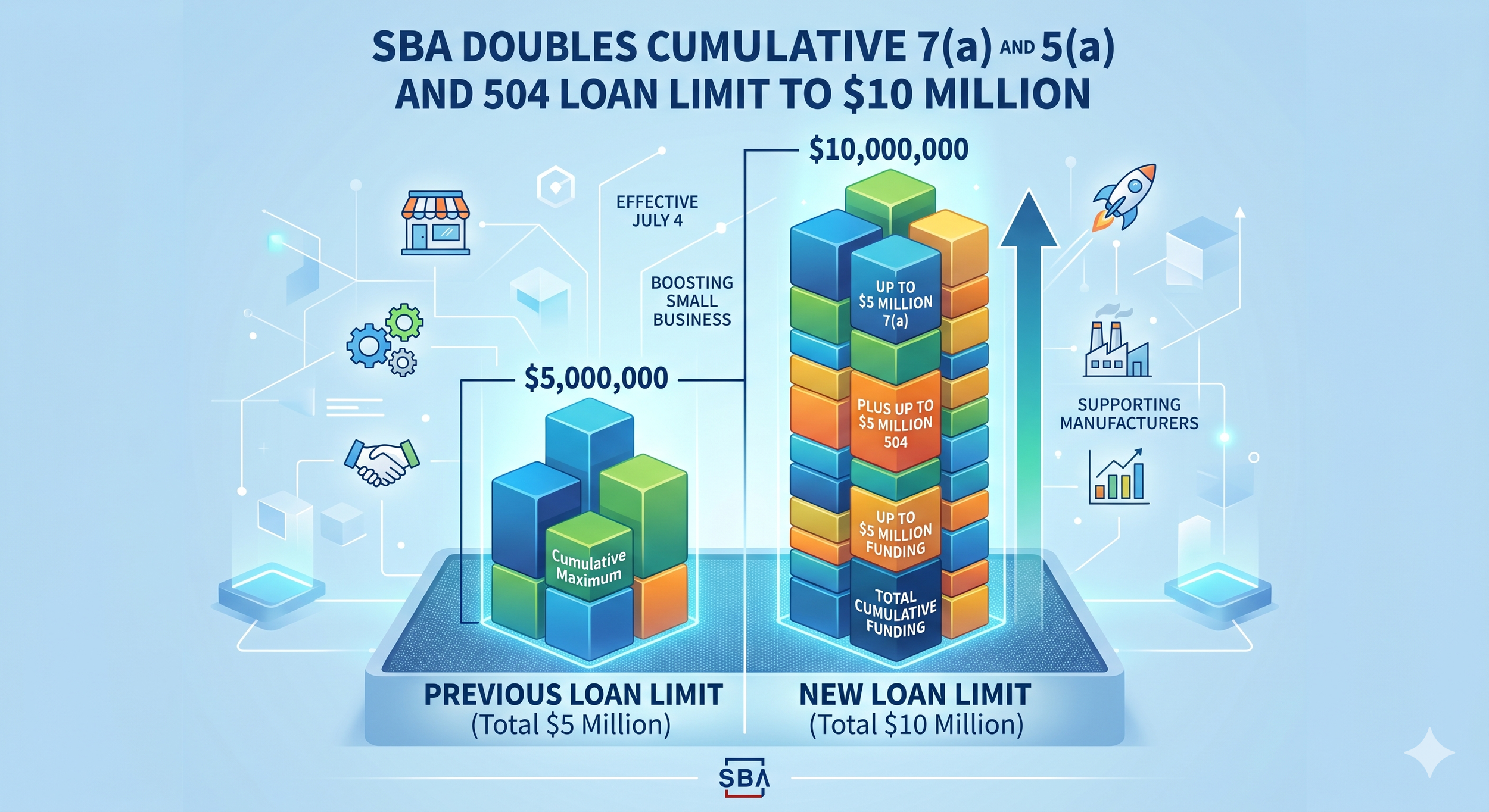

SBA Doubles Cumulative 7(a) and 504 Loan Limit to $10 Million

Effective July 4, eligible borrowers can access record levels of SBA-backed funding

This new SBA rule represents a significant shift in how small businesses, particularly those in capital-intensive industries like manufacturing, can access federal funding.

Here is the consolidated breakdown of the announcement:

The Core Change: Higher Funding Limits

Effective Date: July 4, 2026.

New Combined Limit: Eligible borrowers can now access up to $10 million in cumulative SBA-backed financing.

Decoupling Programs: Under the new rule, the SBA is decoupling 7(a) loan balances from the 504 program. This means a single business can secure a $5 million 7(a) loan and a $5 million 504 loan simultaneously.

Specific Impact on Manufacturers

Expanded 7(a) Access: Small manufacturers (who already had access to unlimited 504 loans for distinct projects) can now also apply for up to $5 million via the 7(a) program.

Fee Waivers: The SBA has waived loan fees for specific manufacturing NAICS codes.

New Guarantees: * 90% Made in America Loan Guarantee: Specifically for small manufacturers.

90% Grocery Guarantee: For small businesses within the food supply chain.

Strategic Objectives

Industry Support: The rule targets capital-intensive sectors including construction, logistics, energy, and food production.

Growth Integration: Allows businesses to pair long-term financing (real estate/equipment via 504) with flexible working capital (via 7(a)).

Economic Context: The move is part of the "America First" agenda, responding to record-high small business formation and a resurgence in domestic manufacturing.

Program Refreshers

Program Primary Use Best For7(a) Loan Equipment, real estate, working capital, and expansion.General business needs and revolving credit.504 Loan Major fixed assets (real estate and long-term machinery).Long-term, fixed-rate financing via nonprofit CDCs.

Note for Homebuilders: The SBA continues to promote the 7(a) Working Capital Pilot (WCP), which provides project-based lines of credit up to $5 million for homebuilders.

View Businesses for Sale that have Bank Financing (SBA Backed) in place for Qualified Buyers.

To qualify as a buyer for an SBA loan, you must satisfy both the SBA's federal guidelines and your lender's specific credit policies.The breakdown of key requirements including but not limited to:

1. Financial "Skin in the Game" (Equity Injection)

A minimum 10% equity injection is generally required for business acquisitions or startups.

This injection must be unborrowed personal cash (savings, 401k rollovers, or seasoned gifts).

The buyer must bring at least 5% of their own cash, though a seller note can cover up to 5% of the total injection.

Any seller note used as equity must typically be on "full standby" (no payments) for the life of the loan.

2. Credit and Character

A personal credit score of 650 or higher is generally needed, with some Preferred Lenders looking for 680+.

Anyone owning 20% or more of the business must provide an unconditional personal guarantee, meaning personal assets like a home can be used for repayment if the business fails.

A clean background is required, specifically a clear record concerning federal debt (no past defaults on student or previous SBA loans) and a clear Statement of Personal History (Form 1919).

3. Management Experience

You must demonstrate industry depth, prove "transferable skills," or show that key management from the previous owner will be retained.

A professional resume detailing your ability to operate the specific type of business being acquired must be submitted.

4. Business Eligibility

The business must be for-profit (non-profits are ineligible for 7(a) loans).

It must meet the SBA's size standards, usually based on average annual receipts or number of employees.

It must operate within the U.S. or its territories.

Ineligible industries for 7(a) loans include gambling, lending, life insurance, and passive real estate investing.

5. Essential Documentation

Three years of personal and business federal tax returns are required.

A personal financial statement (SBA Form 413) and interim business financial statements (P&L and Balance Sheet) dated within the last 120 days are needed.

A detailed business plan is mandatory, especially for startups, and must include two years of financial projections to prove the Debt Service Coverage Ratio (DSCR).

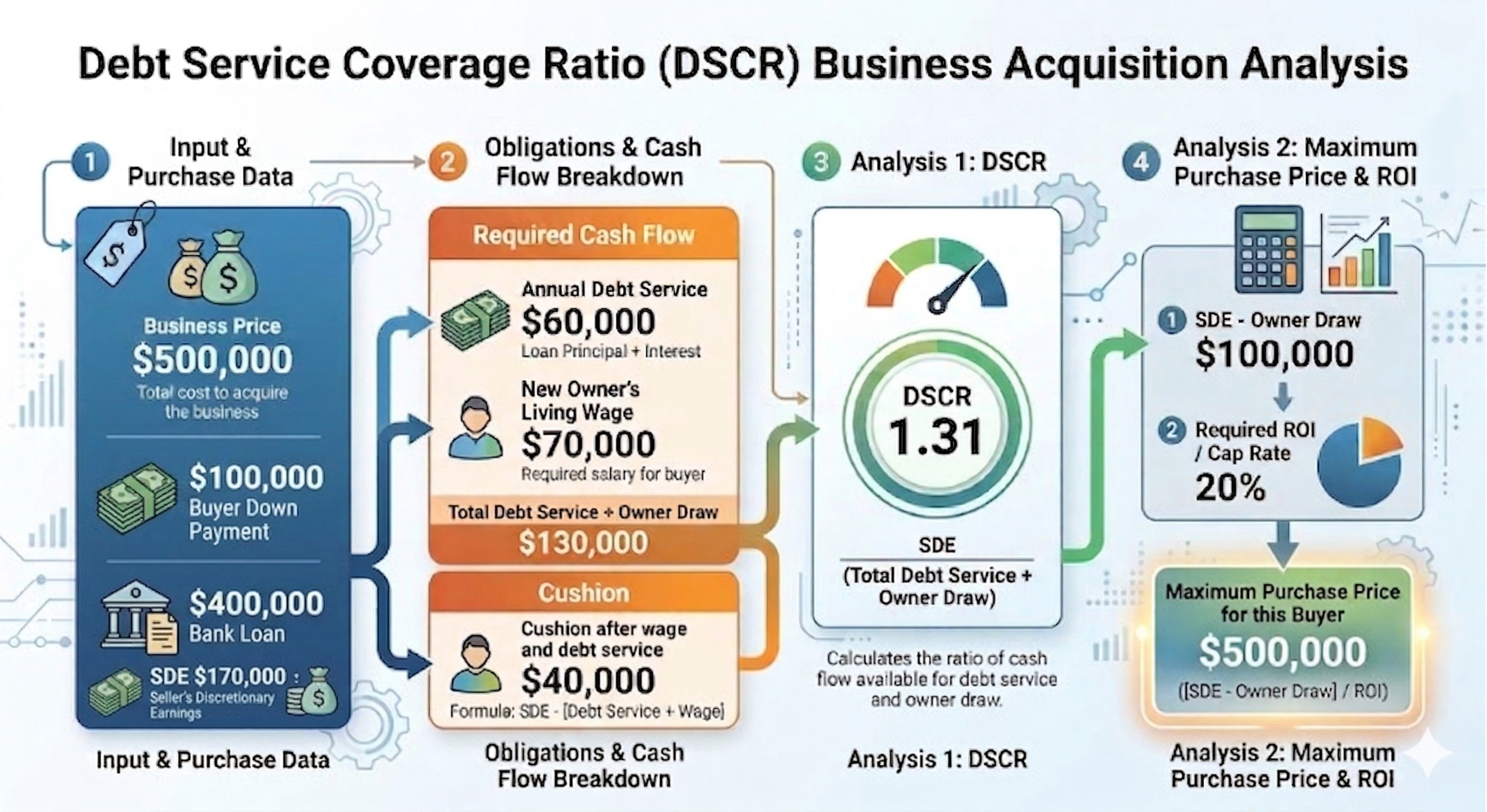

What is Debt Service Coverage Ratio / DSCR and how does this affect your ability to finance a Business Acquisition?

When a acquiring an Owner Operated Business, the Debt Service Coverage Ratio (DSCR) is a critical financial metric used by SBA Backed lenders to determine if a business generates enough income to cover the debt service, plus a market wage Managers Salary (must be enough to pay buyers living expenses / Household expenses) Plus a buffer of 25% to 50%.

Example Graphic Below

Business Price $500,000 Discretionary Earnings $170,000 Annual Debt Service $60,000 + New Owners Living Wage $70,000 = $130,000

Divide SDE $170,000 by $130,000 (Debt Service and Buyers Wage) = 1.30 DSCR

Another way to look at this is

SDE $170,000 - Buyers Wage $70,000 = $100,000

then Divide $100,000 by 20% = $500,000 is the Most a Buyer that needs $70,000 to live on and $60,000 for Debt Service can pay for this business.

The DSCR Formula: The DSCR Formula: Seller Descretionay Earning {SDE} \ Annual Debt Service + {Owner's Living Wage}) = DSCR